Receiving a windfall changes your financial situation overnight. There is a lot of opportunity that exists in these events, but many challenges as well. Many recipients of a financial windfall act too quickly or become paralyzed and fail to take any action at all. What is the proper way to respond to receiving a windfall?

What exactly is a windfall? A windfall is a sudden receipt of assets (often a large amount), sometimes expected and sometimes not.

Common sources of financial windfalls are:

Inheritance or Gifts

Legal Settlements

Business Sale

Gambling Winnings

Stock Liquidation

In all these cases, assets become liquid and available to the recipient quickly and usually change their net worth and ability to give, spend, invest, etc.

So, you get a phone call that you’re receiving millions of dollars, what could go wrong from that? You would think it would be simple, but many financial planners have seen clients spend down or squander windfalls at alarming and surprising rates. Lavish spending habits, large unreasonable purchases, unrealistic expectations of what that level of wealth affords, and lack of a foundation in values all can lead to pitfalls and missteps with found wealth.

How can we navigate receiving a large sum of money in the most prudent way possible? Here are a few ideas:

Don’t change anything right away. Many windfalls involve life changing money, but a dramatic lifestyle change, or large expenditures may jeopardize the sustainability of those funds in a long-term plan. In general, money received from a windfall, especially inheritances, gambling winnings, or settlements, is spent more easily than money that is earned, saved and invested over decades. You see this in the fact that one third of lottery winners go bankrupt within five years. 78% of NFL players face financial hardship and nearly 16% go bankrupt after leaving the league. In the case of inheritance, only 10% of wealth passes to a third generation. The best thing you can do when you receive a windfall is pause until you make a thoughtful, values driven plan.

Understand your emotions. This one may seem irrelevant, and you may be asking, “isn’t this a financial post?” The human element is incredibly important to navigate. In the case of a legal settlement, you may feel relief. In the event of an inheritance, you may feel guilt, anxiety, confusion and sadness. If you win the lottery, it may be ecstasy followed by disbelief. None of these would be abnormal, but your feelings are unique to you and those feelings could be pointing to values that direct decisions yet to come. Listen to how you feel.

Anchor to values. A value is a standard or judgment that you use to determine what is important in your life. While some values like life and freedom are universal, most are relative and vary from person to person. If you value something, it likely won’t change if you are worth $500,000 or $50,000,000. How you address those values could change dramatically. Perhaps championing the homeless or protecting the environment were causes that mattered greatly to you. They will likely still matter to you after the windfall, but how you address them and support them within your financial plan can change. The money changes your plan, it shouldn’t change your values.

Understand what you received and the taxation of that asset. Taxes are a huge expense throughout your lifetime. A business sale could be a huge taxable event, while an inheritance from parents may result in next to no taxes. The taxation of your newfound money varies greatly depending on the source and the vehicle. Understanding what you have after taxes is key. In some cases, like installment sales of a business or the receipt of an IRA, you can spread out some of the tax liability and benefit from ongoing planning. Don’t charge ahead planning on a pretax amount as that will only lead to disappointment when the after-tax amount arrives.

The only timing is your own. Should your portfolio be allocated differently at $20 million versus $200,000? Maybe. If you receive a large sum, can you buy that new car? Probably. Can you spend more monthly with your annuity payout? Most likely. When should you do this? After you take a few weeks to a few months to pause, recenter on your values and build a plan, there is no timeline. Your plan may require a portfolio overhaul. Your ability to retire may move up by a decade. You may be able to gift a large sum to a charity. If your plan is built on the alignment of your newfound capital to your values, the only timing that matters is when you are confident and ready. Important parts of the financial plan would include:

With every source of windfall this is different as they all involve different emotions. In a business sale or settlement, maybe it’s weeks. With the loss of a loved one, maybe it is months or even years. Make a plan with a trusted advisor that allows you to take the time you need to make these decisions, most of which are brand new to you.

Financial windfalls are life changing. Do not let the stress of decision making overwhelm you to the point of inaction. On the opposite side of the coin, do not let the newfound purchasing power let you slip into outspending what you truly value. A financial plan is important for every family and in this case, it is invaluable. If you encounter a windfall, make a plan before you make financial moves.

The Federal Reserve has become pretty transparent about the intentions to raise and cut interest rates. This past month, they implemented the first rate cut of half a percent with the intent to drop rates from 5.5% down to 3% by mid-2026. For those waiting to refinance their mortgage or get a car loan, this is great news. For those who have had their money parked in CDs and money markets, this means the party is over and beating inflation risk free is back to being the myth it has always been.

You can expect is that your high yield account rate will start to drop along with your money market yields. When you go to reinvest your CD proceeds, you will likely find yourself buying a new certificate with a much lower rate attached. For some, this may sound apocalyptic, for others it may not be a big deal. Regardless, how should you approach your safe dollars with rates on their way down?

Seems like a timely question, but the answer is more timeless than what you may think. You keep the funds you will spend in the next three years in cash and invest the rest. This was actually what we were encouraging clients to do when interest rates were at their peak. Interest rates can fluctuate, but with time, cash always loses to inflation. Furthermore, any rate attached to cash vehicles is simply a “rental” of that rate- more on this later.

How much should you leave in cash (CDs, high yield accounts, money markets)?

For accumulators (people actively saving for retirement or another goal), your cash should consist of 1) your emergency funds equal to 3-6 months of expenses and 2) money that will be spent in the near term on a car, a vacation, a home downpayment, etc.

For retirees or those spending down their savings, cash should be equal 3-4 years of living expenses to hedge against sequence of return risk (the risk of having a few bad market years in a row early on in retirement).

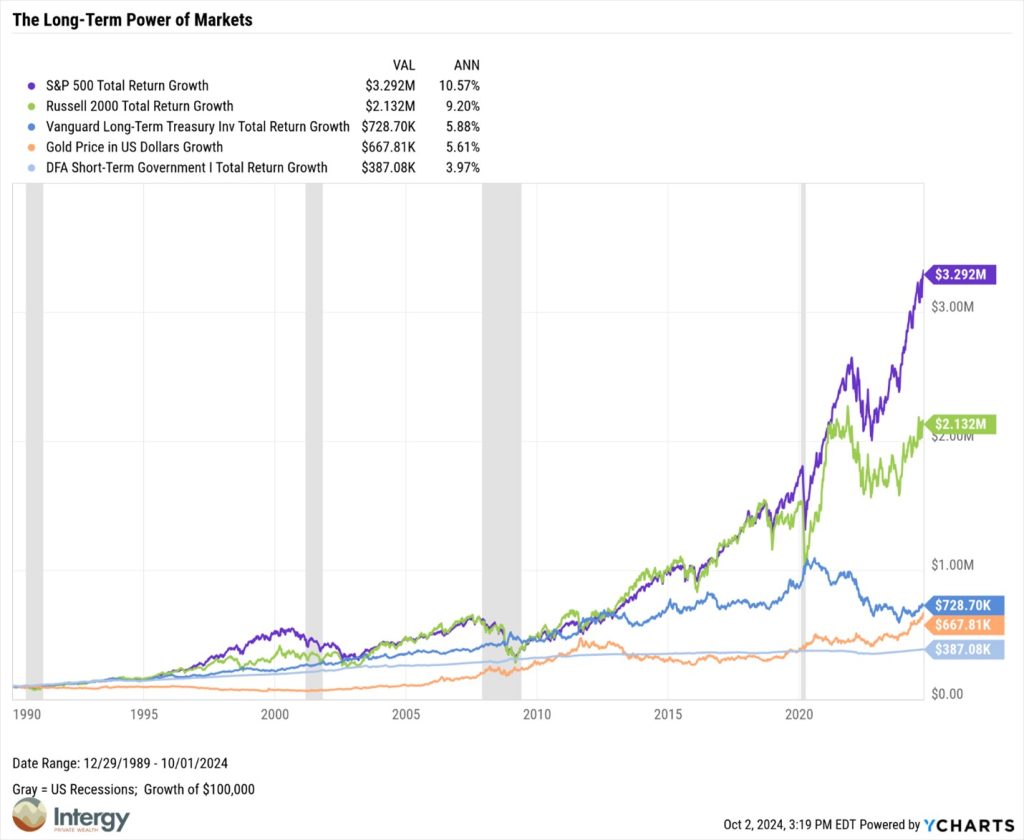

Anything above these amounts should be considered mid to long term dollars and should be assigned a more specific job in the overall portfolio. As you can see in the chart below, the rates of short-term treasuries since 1990 sits below 4%, large cap stocks, small cap stocks, and long term treasuries offered 10.57%, 9.2% and 5.88% respectively. Even gold outperformed what cash and short-term treasury bonds would have offered. You must know why you have the cash, and then make good decision to move money that should not be in cash to other planning and investment goals.

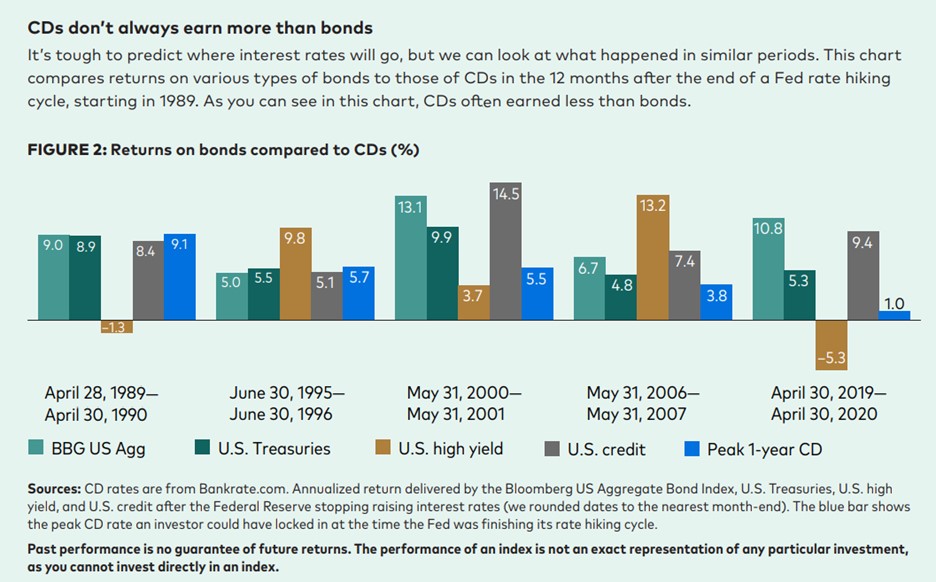

You are renting your interest rate in cash. The same could be said for short term bonds. These are very sensitive to interest rate changes so when rates drop, your interest will respond soon after. Intermediate and long-term bond’s interest rates do not change as quickly. If you own a 10-year bond that pays 5%, it will still pay 5% after the Fed announces a cut or hike. The price may be temporarily affected, but the coupon the bond pays remains the same. If the fixed income portion of your portfolio is meant to sustain a level of income, the time may be right to go from cash to a more sustainable strategy like intermediate and long-term bonds or annuities. Vanguard created the chart below that shows what happens when the Fed finalizes a hiking cycle and, in most periods, you can see that CDs underperform other fixed income securities. So even if you do not want to invest in stocks, there is historical precedent for considering alternatives to cash in the fixed income space.

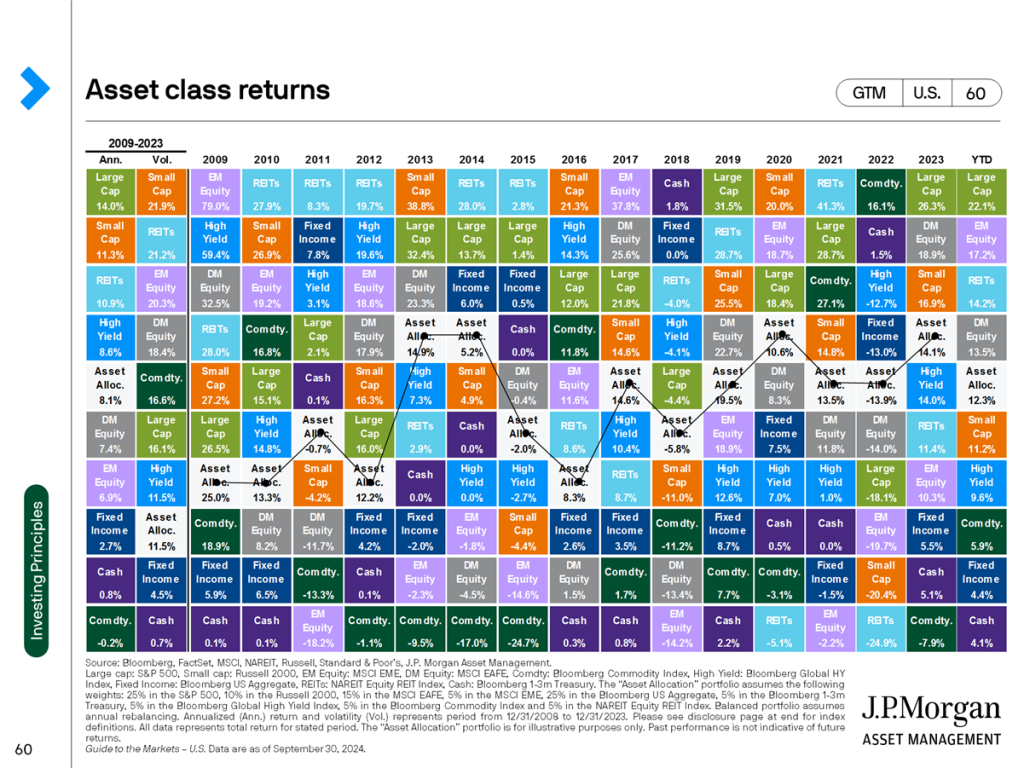

The alternative to bonds and insurance products like annuities is the stock market. You could lean towards the market stalwarts that offer dividends and decades of performance records, or you could go with more growth-oriented companies with high valuations that are pushing innovation. Either way, the performance over time in stocks far outpaces what cash can offer. The tradeoff here is volatility day to day. Look at the quilt below (I know it’s a bit overwhelming to look at, but bear with me).

The 15-year return on cash was 0.8% only beating out commodities. While the average for stocks varied from 6.9% to 14% over the same period. What did you have to put up with? Years like 2011 and 2022 where most stock asset classes were negative. “History provides crucial insight regarding market crises: they are inevitable, painful and ultimately surmountable.” -Shelby Davis

The final question, how do you know how much cash to reposition and where to put it?

“All financial success comes from acting on a plan. A lot of financial failure comes from reacting to the market.” -Nick Murray

So… make a financial plan! A financial plan will help you clarify how much cash to keep parked on the sidelines and how much to put to work. A financial plan will provide clarity while keeping your values front and center. Maybe it is bonds, maybe it is stocks, maybe it is to pay off debt? With rates on the move, it is a great time to start a plan, put cash to work, and build confidence about your future.