A 529 Account is a powerful savings vehicle for education specific goals. Historically, the primary criticism of this account was the lack of flexibility. Penalties and taxes for non-qualified withdraws made some savers shy away while others simply didn’t want to commit to saving money to pay for a four-year institution when they have no idea what their newborn baby’s goals will be in 18 years. While the account still has more limitations than most, a lot of legislative progress has occurred the past several years to make these accounts more flexible and practical to the average American saver. Changes include qualified withdraws for trade schools, qualified withdraws for private K-12 schools, and student loan repayment. The most drastic and noteworthy is the ability to roll funds from a 529 to a Roth IRA.

This new feature has a lot of investors rethinking the 529 Account. Here is what you need to know about rolling your education account into a Roth IRA:

The 529 account must have been open for more than 15 years.

This one is pretty self-explanatory. If you are starting a 529 account for an older child, know that this 15-year period must be satisfied before you can roll funds from the 529 into a Roth IRA. If you start an education account for your 15-year-old, they will be 30 when you can roll over the unused funds.

The funds must be rolled over to a Roth IRA owned by the 529 account beneficiary.

Here’s an example: If your son is the 529 beneficiary, the Roth IRA must also be owned by your son. You can change a beneficiary on a 529 account, so if the funds are meant to be directed to a certain family member, ensure the 529 is matched to their Roth IRA.

There are no tax consequences or penalties when a 529 plan beneficiary is changed to a member of the beneficiary’s family. Qualified family members include the beneficiary’s:

Spouse

Son, daughter, stepchild, foster child, adopted child or a descendent

Son-in-law, daughter-in-law

Siblings or step-siblings

Brother-in-law, sister-in-law

Father-in-law, mother-in-law

Father or mother or ancestor of either, stepmother, stepfather

Aunt, uncle or their spouse

Niece, nephew or their spouse

First cousin or their spouse

The rollover amount cannot exceed the annual IRA contribution limits.

In 2024, this is $7,000. So, no more than $7,000 can go into the account AND this counts as the 2024 contribution. You may be familiar with 401(k), TSP, or 403(b) rollovers which are not subject to the annual contribution cap. The 529 rollover does not adhere to the same logic.

In addition to this counting as the year’s contribution, the beneficiary must have earned income to match or exceed the amount being transferred. If the beneficiary only earns $5,000 at a part time job that year, only $5,000 can be transferred. If they earn $7,000 or more (in 2024), the full annual contribution can be rolled over.

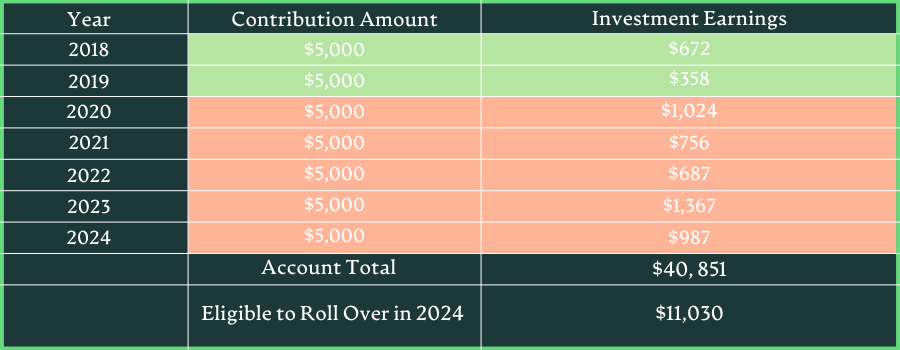

The eligible rollover amount must have been in the 529 account for at least 5 years.

This is a reason to open 529 accounts while your kids are in grade school even if you plan on only funding them minimally. A big thing to understand with this rule is how it works with the 15-year rule. You may have had the account open for 15 years, but most of the funding occurred in the last five years. This means all contributions and investment growth is ineligible to roll over to a Roth IRA until it has been in the account for five years.

This chart is an example of how the 5-year rule would affect your ability to roll over funds in 2024. It is important to note that in 2025, 2020’s contributions and earnings would be freed up to roll into a Roth IRA as well.

There’s a $35,000 lifetime cap on Roth IRA rollovers for each 529 account beneficiary.

At the current rate, that is replacing 5 years of your child's contributions. If they are working and can save $7,000 as well, they can put that in a 401k, HSA, or brokerage account. It is likely that the lifetime cap will increase over time, much like the Roth IRA contribution limits have, but that is not a guarantee.

Roth IRA income limitations are waived for 529-to-Roth IRA Rollovers.

No need for backdoor 529 rollovers. Thank goodness as what a mess that could have been! This could be a planning factor if your beneficiary finds themselves in a high income earning job out of high school or college or if you would like gift money to children or grandchildren in a tax efficient manner.

If you're concerned about the assets in an overfunded a 529 plan, you already have other options. Parents and grandparents can switch designated beneficiaries at any time and continue using a 529 account for qualifying educational purposes. Your first child chooses not to go to college, no worries, change the beneficiary and use the funds for your second. Plus, up to $10,000 of 529 plan funds can be used to pay off qualifying student loans. If you’re trying to remove money from a 529, take a student loan of $10,000 and then withdraw $10,000 to pay off the loan immediately. Finally, if the child earns a tax-free scholarship, parents can take an equivalent amount out of the 529 plan without the 10% penalty (though the earnings portion of the distributions will be taxable). This exception for distribution extends to your child going to a US Service Academy or receiving an ROTC scholarship.

529 Plans should still be viewed as education specific accounts and fairly limited as to their scope. This rule along with other recent additions have made the accounts more attractive and less restrictive. Overall, most savers should still view these new additions as potential backup plans for unplanned windfalls, scholarships, or overfunding rather than a direct retirement savings plan.

If you have a large portion of your annual compensation in the form company stock, you may have heard of an 83(b) election. Some view it as a taboo topic, while others who have had success with the strategy may preach it like it should be blanket advice. What is it and is it something that should be a part of your financial plan?

What is an 83(b) election?

An 83(b) election is a US tax provision that gives an employee the option to pay taxes on the total fair market value of restricted stock at the time of granting rather than the time of vesting. This election relates specifically to Employee Stock Options and Restricted Stock Awards (not Restricted Stock Units). You pay taxes now at a known rate, rather than in the future at an unknown rate and an unknown value.

Why would you consider an 83(b) election?

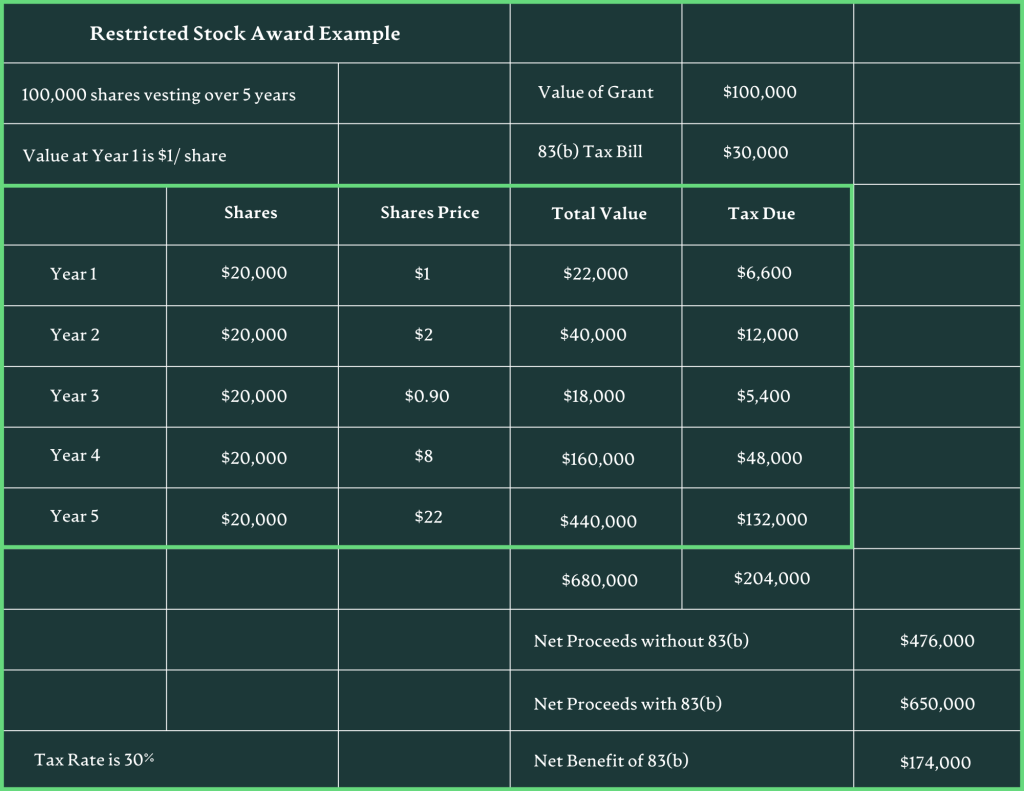

The primary case for an 83(b) election is to pay the tax liability on stock with a lower value in belief or hope that the stock will appreciate and the overall tax effective tax liability on that ownership stake will be much lower. Below is an example:

An employee is granted 100,000 shares of Restricted Stock Awards at the time of their hire. The value of the unvested stock is $100,000. If tax was owed today at a 30% bracket, the employee would have to come up with $30,000 for taxes, not a small sum. Hypothetically, over the five-year vesting period, the stock appreciates, if the 83(b) was selected, it would have saved $174,000 in taxes for this employee. A massive benefit and potentially a life-changing amount of money that would have gone to taxes otherwise.

An 83(b) is most commonly used in one of two instances:

Startups or small businesses. Stock prices in these instances are usually very small which can make the tax bill more manageable and gives the stock price tremendous upside. When a company reaches a certain size, outsized growth is difficult to achieve. As a small company, it is possible to triple and quadruple the business income and value every year. This makes options and stock awards in a smaller sized company as a target for the 83(b) election.

Large downward stock movement. I am not talking about a 5% drop in your company’s stock price. I am referring to a black swan type event within your company. The drop could be 40% or more. In this case, the value of the stock now is lower than when it was granted and in the case of a recovery, your tax bill could be dramatically reduced by electing an 83(b).

You may be in one of those groups and now think, “wow, an 83(b) is a no-brainer, a complete layup, I will do it immediately.” Slow down a bit. While it presents an amazing planning opportunity and potentially life changing tax savings, it does have some risks and downsides.

Here are the potential downsides of an 83(b) election:

The first is very practical, you must have the cash to pay the taxes! If you project out the life of the options or the awards, you could see hundreds of thousands of tax savings, but the current tax bill is still the current tax bill. Without that amount of money, this is not an option. If you have excess savings, the ability to access a loan responsibly, or a family member with the ability to gift you the money, then you know the tax funding is secured and you can move on to other considerations.

The startup goes bankrupt. Depending on the study you read, somewhere in between 75-90% of startups fail within the first five years of operations. So, for every success story, there are 8 or 9 stories of failure. The risk of exercising an 83(b) election in year one of your startup is that those awards and options may be worth zero by the time you vest, and you are left with a negative after-tax return on the ownership of that stock.

The stock price never recovers. If your stock is more mature and you elect in a market dip, the positive outcome requires the stock price to bounce back and exceed the prior high. JP Morgan has estimated that since 1980, 40% of all stocks in the Russell 3000 dropped by 70%+ and never recovered. The drop became permanent. If an 83(b) election was chosen, you paid tax today and lost that value for a benefit that will never be seen.

You leave the company before you vest. Once you pay the tax bill, the US government does not care if you actually vest in the stock. Leaving before your vesting will result in taxes paid on shares of stock that were never received. An 83(b) election will limit your career flexibility during your vesting period if you want to maximize the full benefit.

Last, is your taxable income outside of the stock awards. In an ideal scenario, you can marry an 83(b) election in a tax year where other income is lower. This could maximize the benefit even more by not only receiving the benefit of a tax bill on a lower valued stock, but also be in a lower effective tax rate. If your income is variable or you have a spouse with a higher income, perhaps the 83(b) can hurt more than help based on the timing.

The 83(b) election allows an employee to pay tax now to receive a potential benefit as their stock appreciates, but the tax bill remains flat. This can be an important strategy for those who receive a large amount of their compensation from Stock Awards and Employee Options and for employees of startups. Like all financial planning, it is incredibly personal, and the suitability can vary from person to person. If you’re at an impasse with your stock benefits, work with an independent CERTIFIED FINANCIAL PLANNER™ to determine what makes sense within your plan and aligns with your values.

This is probably one of the most frequent questions I get from clients and prospective clients. With the rise in mortgage rates the past 18 months, it is more relevant now than ever. So, should you pay off your mortgage early?

I believe this question has two parts. The first effects the second, but ultimately, the second part is the final decision maker.

First is the math of it all.

Second is the feelings of it all.

So, the math. According to the Apollo Group, 61% of outstanding mortgages are below 4%. So we can use 4% as a decent base case.

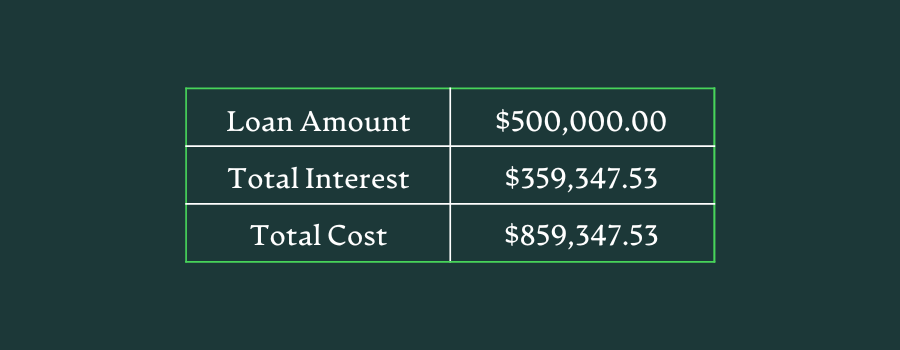

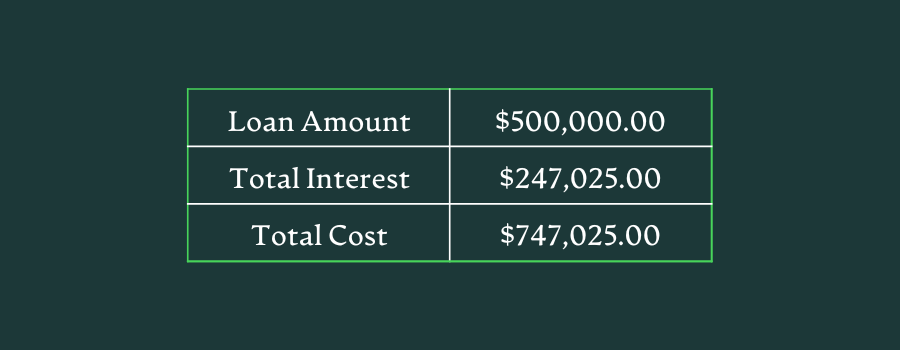

Let’s buy a $500,000 house using a 30 year mortgage. Not including taxes and insurance (because you will pay those regardless), your monthly payment would be $2,387. By paying exactly according to schedule, you would have paid:

Not too bad. But now, enter the question, “I have $500 extra per month, should I save, invest or pay off debt?”

How much interest do we save over the life of the loan by paying an extra $500 per month?

You would have lowered your 30 year mortgage to 21.5 years and your new loan cost would be:

A savings of 8.5 years of cash flow and $112,322.53 off the 30 year schedule. Not too bad at all, actually pretty great, but can we do better?

Two alternatives are to save and invest the money.

For saving, we will use a rate of return of 4%, similar to many high yield savings accounts.

For investing, we will assume a rate of return of 7.5% which is the average annual return of a 70% stock, 30% bond portfolio over the past 21 years.

The question we are looking for in these alternatives is, if we choose one and stick with it for the same timeframe as our projected mortgage payoff, do we net out more?

Savings Scenario- 4% Rate of Return $500/m contribution for 259 months

$500 per month into your high yield savings account would have grown to $204,822 after 259 months.

Investment Scenario – 7.5% Rate of Return. $500/m contribution for 259 months

A $500 per month contribution investment portfolio of 70% stocks and 30% bonds would have grown to a balance of $323,729 after 259 months (21.5 years).

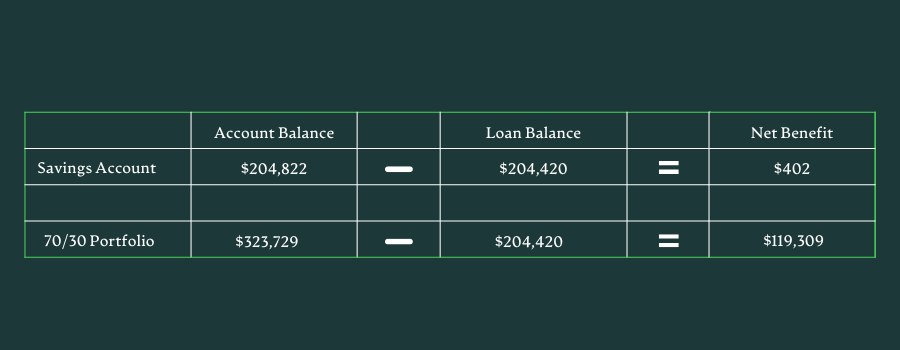

Assuming you are paying your mortgage according to schedule in both scenarios, after the 259th month, you would still owe an outstanding balance of $204,419.

If we want the house paid off in 21.5 years, here’s what it looks like:

So, saving the difference netted you $402 over 21.5 years or just over $18 per year. Maybe not worth it, especially since rates on savings accounts can change much more easily than rates on your mortgage. Bottom line, a savings interest rate close to your mortgage rate is a draw. If you value flexibility, cash savings could be the answer. If you like the knowns and certainty, pay off the debt as the interest is a known cost.

What is compelling is investing. The $119,309 swing is significant and could change your financial situation quite a bit. Historically, the more stocks you move into the allocation, the better your long-term return, but the unknown of future returns is the tradeoff for the clear opportunity. The bottom line here is, if you have the time, the opportunity of the stock market is attractive. A shorter pay-off window means less time in the market which means more variability of outcomes both good and bad. By that I mean, when investing for shorter periods, you could potentially end up with a plus 41% return just as likely as you could get a 7% return or a negative 25% return.

On top of both of these scenarios, you now have 8.5 years to save and invest what you were paying for your mortgage. So take that leftover investment account of $119,309. Now that your mortgage is paid, add the $2,387 per month and at the end of the original 30 year period, you could have a $560,612* account. Not bad at all.

*all based on a 7.5% market return estimation*

Big factors to consider for the math part:

Mortgage Interest Rate

Time left on the mortgage (or time you’d like to have it paid off by)

Alternative savings or investment return

So, the math part is good to go. Now, to quote the philosophical film, The Notebook, “What do you want?”

If the Milky Way Galaxy was your lifetime of your decisions, the financial and mathematical decisions would be something like Earth. Yeah, we humans are big fans of earth, but given the entire galaxy, there is a lot more to it. The other planets, all of the stars, the black holes that creep us all out a bit, the moon, the sun! There is a lot more to it. Math drives some financial choices, but in the scheme of your life you likely make most of your choices by something other than mathematical sense. Values, purpose, religion, profession, family, even selfishness all drive decisions that no math or even reason could combat.

Some questions to help us figure out what we want…

Is debt crippling to us?

Why do we view debt in a negative or indifferent light?

How were we raised to think about debt?

Does being debt free sooner rather than later affect the outcome of my long-term vision?

Is being debt free a goal that ranks higher than others according to what I truly value?

Everyone’s answers to these will be different. After all, personal finance is… personal.

If you have anxiety when you think about debt and would live a happier life being debt free, perhaps it is prudent for your lifestyle to paydown the mortgage sooner rather than later. Maybe you appreciate the opportunity to earn more appreciation and income elsewhere like the stock market or a business so you forgo the repayment of the debt for flexibility and appreciation. Decide what really matters to you.

Once you know what you value today and where you want to be tomorrow, bring the math back in and make the best decision to support that. In reality, a plan that does not support your abilities and peace of mind today is ill suited to accomplish your goals in the future.

Factors to consider for the feelings part:

Feelings toward debt

Long term vision

Need for flexibility

Desire to maximize opportunity

Family values

Wrapping up with the original question, “Should I pay off my mortgage early?”

It truly depends. Based off your interest rate and the time you are shooting for, work with someone who will help you figure out the math of it all and then listen to you as you sort through the “what do you want?” question.

A 529 Account is a powerful savings vehicle for education specific goals. Historically, the primary criticism of this account was the lack of flexibility. Penalties and taxes for non-qualified withdraws made some savers shy away while others simply didn’t want to commit to saving money to pay for a four-year institution when they have no idea what their newborn baby’s goals will be in 18 years. While the account still has more limitations than most, a lot of legislative progress has occurred the past several years to make these accounts more flexible and practical to the average American saver. Changes include qualified withdraws for trade schools, qualified withdraws for private K-12 schools, and student loan repayment. The most drastic and noteworthy is the ability to roll funds from a 529 to a Roth IRA.

This new feature has a lot of investors rethinking the 529 Account. Here is what you need to know about rolling your education account into a Roth IRA:

The 529 account must have been open for more than 15 years.

This one is pretty self-explanatory. If you are starting a 529 account for an older child, know that this 15-year period must be satisfied before you can roll funds from the 529 into a Roth IRA. If you start an education account for your 15-year-old, they will be 30 when you can roll over the unused funds.

The funds must be rolled over to a Roth IRA owned by the 529 account beneficiary.

Here’s an example: If your son is the 529 beneficiary, the Roth IRA must also be owned by your son. You can change a beneficiary on a 529 account, so if the funds are meant to be directed to a certain family member, ensure the 529 is matched to their Roth IRA.

There are no tax consequences or penalties when a 529 plan beneficiary is changed to a member of the beneficiary’s family. Qualified family members include the beneficiary’s:

Spouse

Son, daughter, stepchild, foster child, adopted child or a descendent

Son-in-law, daughter-in-law

Siblings or step-siblings

Brother-in-law, sister-in-law

Father-in-law, mother-in-law

Father or mother or ancestor of either, stepmother, stepfather

Aunt, uncle or their spouse

Niece, nephew or their spouse

First cousin or their spouse

The rollover amount cannot exceed the annual IRA contribution limits.

In 2024, this is $7,000. So, no more than $7,000 can go into the account AND this counts as the 2024 contribution. You may be familiar with 401(k), TSP, or 403(b) rollovers which are not subject to the annual contribution cap. The 529 rollover does not adhere to the same logic.

In addition to this counting as the year’s contribution, the beneficiary must have earned income to match or exceed the amount being transferred. If the beneficiary only earns $5,000 at a part time job that year, only $5,000 can be transferred. If they earn $7,000 or more (in 2024), the full annual contribution can be rolled over.

The eligible rollover amount must have been in the 529 account for at least 5 years.

This is a reason to open 529 accounts while your kids are in grade school even if you plan on only funding them minimally. A big thing to understand with this rule is how it works with the 15-year rule. You may have had the account open for 15 years, but most of the funding occurred in the last five years. This means all contributions and investment growth is ineligible to roll over to a Roth IRA until it has been in the account for five years.

This chart is an example of how the 5-year rule would affect your ability to roll over funds in 2024. It is important to note that in 2025, 2020’s contributions and earnings would be freed up to roll into a Roth IRA as well.

There’s a $35,000 lifetime cap on Roth IRA rollovers for each 529 account beneficiary.

At the current rate, that is replacing 5 years of your child's contributions. If they are working and can save $7,000 as well, they can put that in a 401k, HSA, or brokerage account. It is likely that the lifetime cap will increase over time, much like the Roth IRA contribution limits have, but that is not a guarantee.

Roth IRA income limitations are waived for 529-to-Roth IRA Rollovers.

No need for backdoor 529 rollovers. Thank goodness as what a mess that could have been! This could be a planning factor if your beneficiary finds themselves in a high income earning job out of high school or college or if you would like gift money to children or grandchildren in a tax efficient manner.

If you're concerned about the assets in an overfunded a 529 plan, you already have other options. Parents and grandparents can switch designated beneficiaries at any time and continue using a 529 account for qualifying educational purposes. Your first child chooses not to go to college, no worries, change the beneficiary and use the funds for your second. Plus, up to $10,000 of 529 plan funds can be used to pay off qualifying student loans. If you’re trying to remove money from a 529, take a student loan of $10,000 and then withdraw $10,000 to pay off the loan immediately. Finally, if the child earns a tax-free scholarship, parents can take an equivalent amount out of the 529 plan without the 10% penalty (though the earnings portion of the distributions will be taxable). This exception for distribution extends to your child going to a US Service Academy or receiving an ROTC scholarship.

529 Plans should still be viewed as education specific accounts and fairly limited as to their scope. This rule along with other recent additions have made the accounts more attractive and less restrictive. Overall, most savers should still view these new additions as potential backup plans for unplanned windfalls, scholarships, or overfunding rather than a direct retirement savings plan.