10/07/2022

Home Buying in 2022

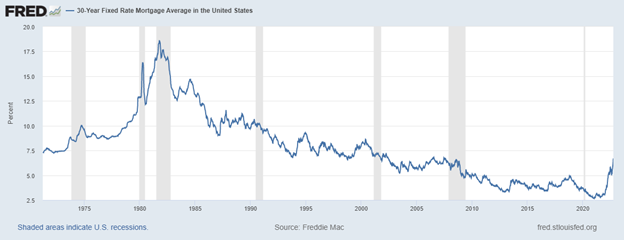

As if buying a home was not tough enough, 2022 has presented a whole new set of issues that potential home buyers must solve. Prior to 2020, the real estate market was healthy, but relatively normal. Demand was high as the economy was in a healthy place, but supply was steady and rates were low historically, but still healthy. Enter Covid 19. Rates are slashed causing the 30 year mortgage to bottom just at over 2.5%- (all time lows). Supply chain shocks disrupted supply while work from home opportunities and stimulus packages caused demand to continue upward. Now rates are rising quickly while demand wains and supply stays low.

So practically, this is how that scenario played out. A house bought in 2019 for $425,000 financed at 3% cost $1,800/m not including taxes and insurance. In 2022, that home is worth about $700,000. So, if interest rates were the same, the monthly payment would be $2,950. Except the average rate has doubled to 6.7% (still below its historic lows- see chart below). That means to buy the same house today, the payment would be $4,520 a month not including taxes and insurance. Nearly $3,000 more than what the payment was less than four years ago. In recent months, home prices around the US have begun to flatten and even drop slightly as demand slows. We will see how that trend plays out over time.

Reading this, you may be distraught, thinking I will never buy a home or a townhome, or a condo or even a trailer for that matter. Worry not, let’s put it in a bit of perspective. The median family household income in the US is $86,372. That is $7,197 gross monthly income. Paying for living arrangements should not exceed 40% by a simple rule of thumb. If buying a home based on the Zillow Home Value Index average, the average earner would buy the average home valued at $354,649. A mortgage payment of $2,290 at today’s rates. That comes to 32% of gross income meaning, with no down payment, it is still feasible for an average income earner to purchase an average home in the US. With taxes and insurance in the equation, the situation is less than ideal, but still doable.

Now that we know that is achievable, here are some things to think about if moving soon or buying a home for the first time:

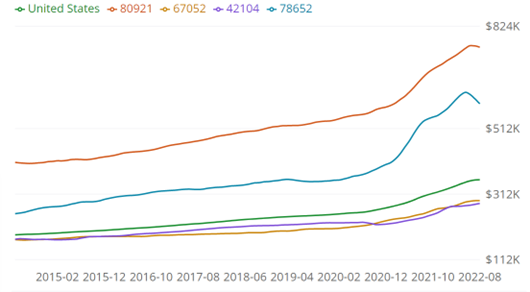

- Manage Expectations: Just like the math I did above, it is important to understand what kind of house you are in the market for. I spoke on national averages, which nearly no one actually faces. Based on where you are geographically that may mean looking for a condo versus a single family. It may mean being in a suburb 15 minutes further than your ideal. Expectations on the front end to help start your home search is a healthy way not to bite off more than you can chew. A simple pro/cons list may help as well- yard size, bedrooms, geographic preference if you are remote, etc. Reference this chart that shows the national average compared to averages in Colorado, Texas, Kansas and Kentucky- all markets are not the same.

- Understand the first home does not have to be the last home: In the era of HGTV and Instagram, we all can fall under the impression that open floor plans, infinity pools, and 5.7 acre lots are basic human necessities. This keeping up with the Jones’ is an endless trap that can quickly have us overspending on features that would be ideal, but are simply not needed. Your household income and savings will likely go up. Interest rates will inevitably fall again. A home purchase is a decision to own for an extended period of time, but not forever.

- Understand financing options: Buy a 30-year mortgage and pay 20% down, right? Not really. For many home buyers can qualify for an FHA or VA loan. These are backed by the government and could have as low down payment requirements as 3.5%- for the VA loan, 0%. For young professionals in the medical, legal, or finance industries (among others), there are “Professional Loans” which acts very much like a 30-year mortgage but requires a low down payment and no PMI (Private mortgage insurance). Talk to a lender early in the process to see if you fall under any of these programs.

- Saving for a down payment: Even with the above programs, the average down payment in the US still sits around 13% of the loan’s value. So how and where do you accumulate that money. First, save alongside your other goals. Continue to use your 401(k) and get your employers match for example. Then set an amount- maybe monthly or maybe all bonus income- to go to a separate account. This account should be a high yield savings account or some sort of FDIC insured cash/ CD account. If the home buying goal is past five years, potentially consider a balanced investment account in conjunction.

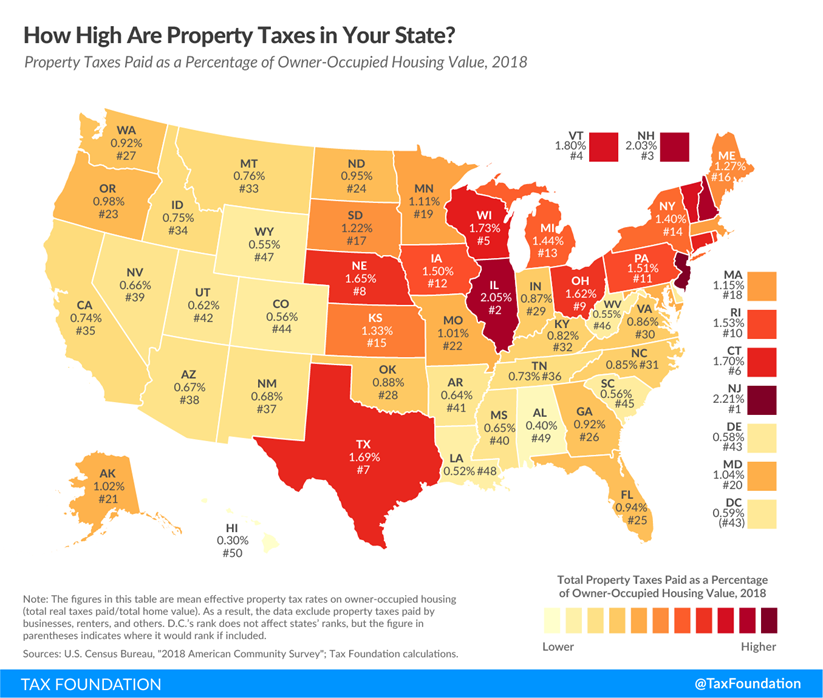

- Plan for the monthly payment: Once you have worked through the above, realize that early on, it is the payment you need to be able to afford. Over time, home prices tend to appreciate slightly above inflation and you will pay off the loan balance. This naturally will lead to positive equity. Lenders often offer you to buy down points to lower the interest rate citing the savings over 30 plus years. In actuality, the length of ownership in the US is less than 13 years, with the number dropping for first time owners. Focus on your plan, the amount you intended to put down and the payment. Flexibility has a value that is tough to quantify. There is no guarantee that interest rates will drop again, but historically there have been swings. If you can afford a home at 7%, you will love it when you can potentially refinance lower a couple years down the road. Last thing here is that geography affects insurance and taxes greatly. Know your expected tax and insurance bill before you start shopping. For example, Hawaii has the lowest rate at.3% while New Jersey has the highest at 2.21%. For a $500,000 house your monthly tax bill would be $125 in HI while it would sit at $921 in New Jersey.

Plan for the unexpected: Finally, and maybe most importantly, is that in home ownership your mortgage payment is the guaranteed minimum you will ever pay monthly. Contrast that to rental payments where your rent is the guaranteed maximum. As a home owner, you get the benefit of interest and tax deductions, property value appreciation and customization. You also take on the responsibility for all repairs, additions, and upgrades that will ever occur to your property. An account like an emergency fund comprising of at least 3-6 months of living expenses is critically important when becoming a home owner.

Buying a home is different now than it was several years ago. Most people do not fall into the situation where they are purchasing a home at the national average and location can make taxes and insurance vary widely. With that, flexibility for workers has changed significantly too. You can work with a global team and it makes little difference if you are in Colorado Springs or New York City or Topeka. No matter the situation, with some planning, many goals can become a reality whether that be over the next month or several years. If you or a family member are considering a home purchase and would like an objective take on your plan, please let our team know.