05/01/2024

Should I Consider an 83(b) Election?

Written by Geoffrey Schaefer, CFP®

If you have a large portion of your annual compensation in the form company stock, you may have heard of an 83(b) election. Some view it as a taboo topic, while others who have had success with the strategy may preach it like it should be blanket advice. What is it and is it something that should be a part of your financial plan?

What is an 83(b) election?

An 83(b) election is a US tax provision that gives an employee the option to pay taxes on the total fair market value of restricted stock at the time of granting rather than the time of vesting. This election relates specifically to Employee Stock Options and Restricted Stock Awards (not Restricted Stock Units). You pay taxes now at a known rate, rather than in the future at an unknown rate and an unknown value.

Why would you consider an 83(b) election?

The primary case for an 83(b) election is to pay the tax liability on stock with a lower value in belief or hope that the stock will appreciate and the overall tax effective tax liability on that ownership stake will be much lower. Below is an example:

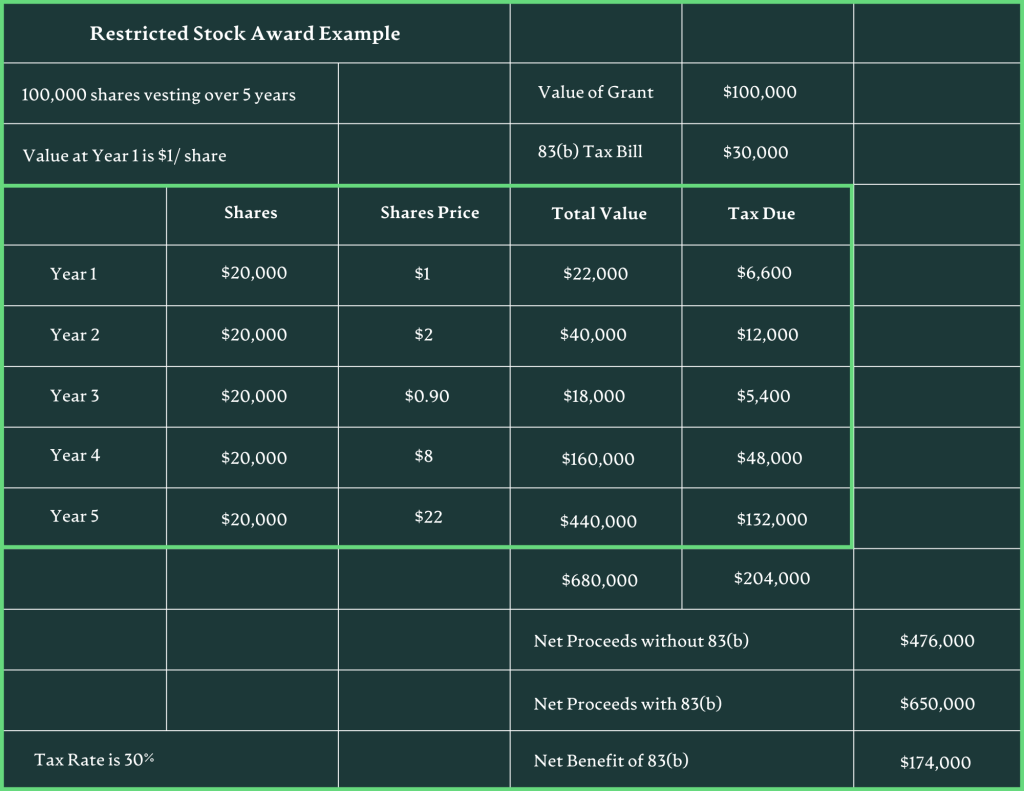

An employee is granted 100,000 shares of Restricted Stock Awards at the time of their hire. The value of the unvested stock is $100,000. If tax was owed today at a 30% bracket, the employee would have to come up with $30,000 for taxes, not a small sum. Hypothetically, over the five-year vesting period, the stock appreciates, if the 83(b) was selected, it would have saved $174,000 in taxes for this employee. A massive benefit and potentially a life-changing amount of money that would have gone to taxes otherwise.

An 83(b) is most commonly used in one of two instances:

- Startups or small businesses. Stock prices in these instances are usually very small which can make the tax bill more manageable and gives the stock price tremendous upside. When a company reaches a certain size, outsized growth is difficult to achieve. As a small company, it is possible to triple and quadruple the business income and value every year. This makes options and stock awards in a smaller sized company as a target for the 83(b) election.

- Large downward stock movement. I am not talking about a 5% drop in your company’s stock price. I am referring to a black swan type event within your company. The drop could be 40% or more. In this case, the value of the stock now is lower than when it was granted and in the case of a recovery, your tax bill could be dramatically reduced by electing an 83(b).

You may be in one of those groups and now think, “wow, an 83(b) is a no-brainer, a complete layup, I will do it immediately.” Slow down a bit. While it presents an amazing planning opportunity and potentially life changing tax savings, it does have some risks and downsides.

Here are the potential downsides of an 83(b) election:

- The first is very practical, you must have the cash to pay the taxes! If you project out the life of the options or the awards, you could see hundreds of thousands of tax savings, but the current tax bill is still the current tax bill. Without that amount of money, this is not an option. If you have excess savings, the ability to access a loan responsibly, or a family member with the ability to gift you the money, then you know the tax funding is secured and you can move on to other considerations.

- The startup goes bankrupt. Depending on the study you read, somewhere in between 75-90% of startups fail within the first five years of operations. So, for every success story, there are 8 or 9 stories of failure. The risk of exercising an 83(b) election in year one of your startup is that those awards and options may be worth zero by the time you vest, and you are left with a negative after-tax return on the ownership of that stock.

- The stock price never recovers. If your stock is more mature and you elect in a market dip, the positive outcome requires the stock price to bounce back and exceed the prior high. JP Morgan has estimated that since 1980, 40% of all stocks in the Russell 3000 dropped by 70%+ and never recovered. The drop became permanent. If an 83(b) election was chosen, you paid tax today and lost that value for a benefit that will never be seen.

- You leave the company before you vest. Once you pay the tax bill, the US government does not care if you actually vest in the stock. Leaving before your vesting will result in taxes paid on shares of stock that were never received. An 83(b) election will limit your career flexibility during your vesting period if you want to maximize the full benefit.

- Last, is your taxable income outside of the stock awards. In an ideal scenario, you can marry an 83(b) election in a tax year where other income is lower. This could maximize the benefit even more by not only receiving the benefit of a tax bill on a lower valued stock, but also be in a lower effective tax rate. If your income is variable or you have a spouse with a higher income, perhaps the 83(b) can hurt more than help based on the timing.

The 83(b) election allows an employee to pay tax now to receive a potential benefit as their stock appreciates, but the tax bill remains flat. This can be an important strategy for those who receive a large amount of their compensation from Stock Awards and Employee Options and for employees of startups. Like all financial planning, it is incredibly personal, and the suitability can vary from person to person. If you’re at an impasse with your stock benefits, work with an independent CERTIFIED FINANCIAL PLANNER™ to determine what makes sense within your plan and aligns with your values.

Follow us on social media