10/04/2024

With Rates Falling, What Do I Do With My Cash?

Written by Geoffrey Schaefer, CFP®

The Federal Reserve has become pretty transparent about the intentions to raise and cut interest rates. This past month, they implemented the first rate cut of half a percent with the intent to drop rates from 5.5% down to 3% by mid-2026. For those waiting to refinance their mortgage or get a car loan, this is great news. For those who have had their money parked in CDs and money markets, this means the party is over and beating inflation risk free is back to being the myth it has always been.

You can expect is that your high yield account rate will start to drop along with your money market yields. When you go to reinvest your CD proceeds, you will likely find yourself buying a new certificate with a much lower rate attached. For some, this may sound apocalyptic, for others it may not be a big deal. Regardless, how should you approach your safe dollars with rates on their way down?

Seems like a timely question, but the answer is more timeless than what you may think. You keep the funds you will spend in the next three years in cash and invest the rest. This was actually what we were encouraging clients to do when interest rates were at their peak. Interest rates can fluctuate, but with time, cash always loses to inflation. Furthermore, any rate attached to cash vehicles is simply a “rental” of that rate- more on this later.

How much should you leave in cash (CDs, high yield accounts, money markets)?

- For accumulators (people actively saving for retirement or another goal), your cash should consist of 1) your emergency funds equal to 3-6 months of expenses and 2) money that will be spent in the near term on a car, a vacation, a home downpayment, etc.

- For retirees or those spending down their savings, cash should be equal 3-4 years of living expenses to hedge against sequence of return risk (the risk of having a few bad market years in a row early on in retirement).

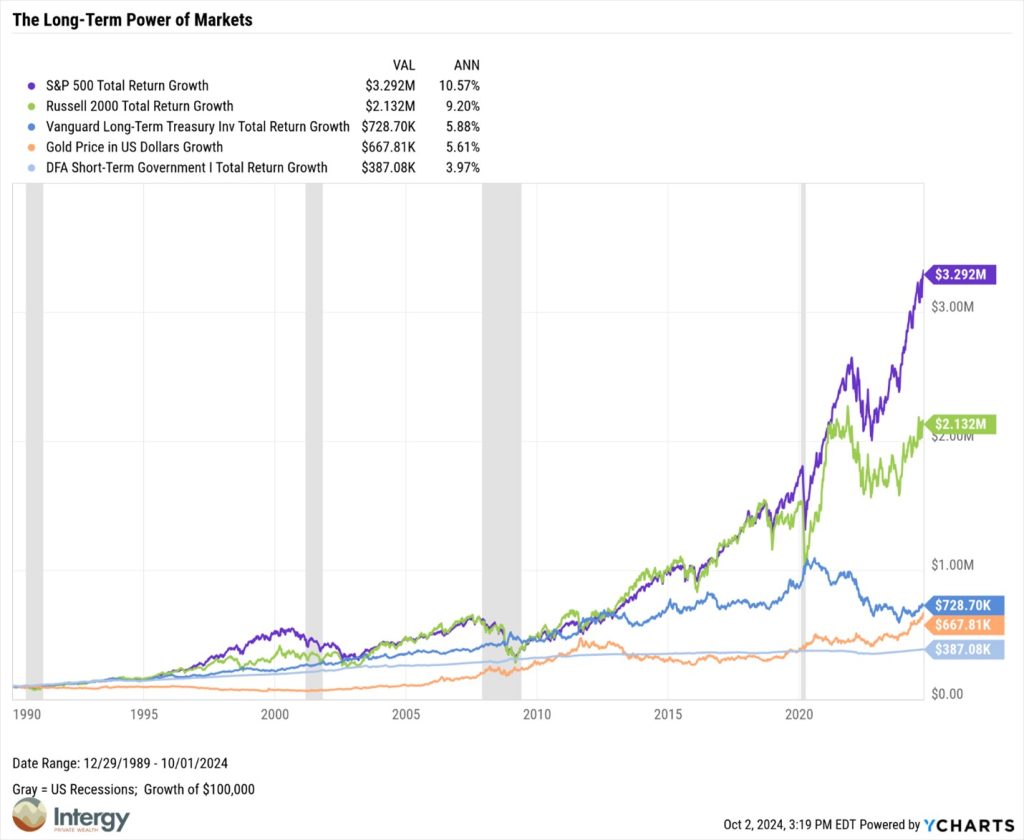

Anything above these amounts should be considered mid to long term dollars and should be assigned a more specific job in the overall portfolio. As you can see in the chart below, the rates of short-term treasuries since 1990 sits below 4%, large cap stocks, small cap stocks, and long term treasuries offered 10.57%, 9.2% and 5.88% respectively. Even gold outperformed what cash and short-term treasury bonds would have offered. You must know why you have the cash, and then make good decision to move money that should not be in cash to other planning and investment goals.

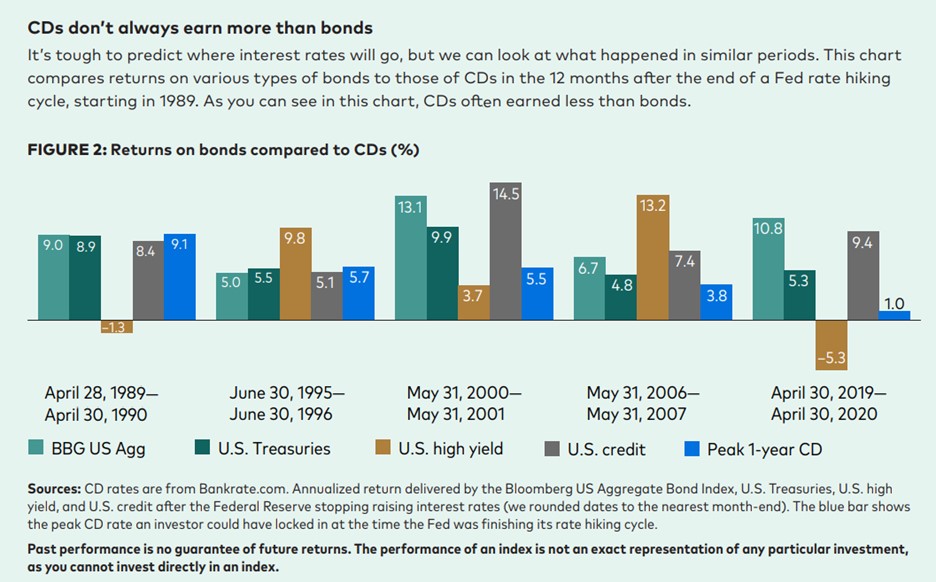

You are renting your interest rate in cash. The same could be said for short term bonds. These are very sensitive to interest rate changes so when rates drop, your interest will respond soon after. Intermediate and long-term bond’s interest rates do not change as quickly. If you own a 10-year bond that pays 5%, it will still pay 5% after the Fed announces a cut or hike. The price may be temporarily affected, but the coupon the bond pays remains the same. If the fixed income portion of your portfolio is meant to sustain a level of income, the time may be right to go from cash to a more sustainable strategy like intermediate and long-term bonds or annuities. Vanguard created the chart below that shows what happens when the Fed finalizes a hiking cycle and, in most periods, you can see that CDs underperform other fixed income securities. So even if you do not want to invest in stocks, there is historical precedent for considering alternatives to cash in the fixed income space.

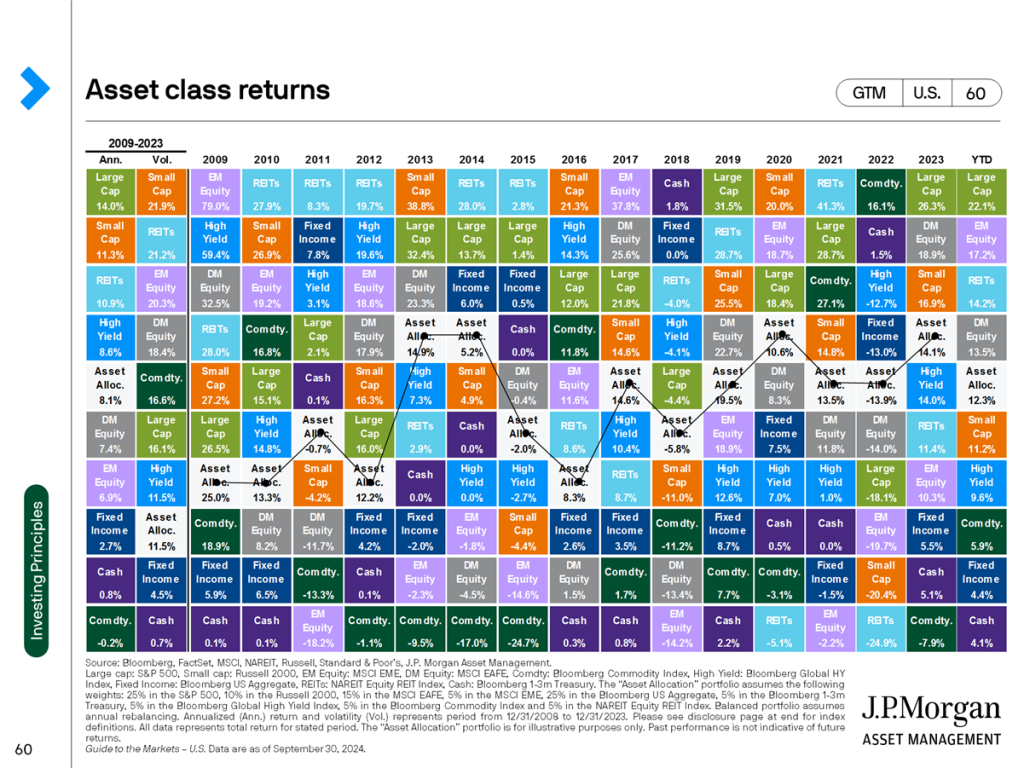

The alternative to bonds and insurance products like annuities is the stock market. You could lean towards the market stalwarts that offer dividends and decades of performance records, or you could go with more growth-oriented companies with high valuations that are pushing innovation. Either way, the performance over time in stocks far outpaces what cash can offer. The tradeoff here is volatility day to day. Look at the quilt below (I know it’s a bit overwhelming to look at, but bear with me).

The 15-year return on cash was 0.8% only beating out commodities. While the average for stocks varied from 6.9% to 14% over the same period. What did you have to put up with? Years like 2011 and 2022 where most stock asset classes were negative. “History provides crucial insight regarding market crises: they are inevitable, painful and ultimately surmountable.” -Shelby Davis

The final question, how do you know how much cash to reposition and where to put it?

“All financial success comes from acting on a plan. A lot of financial failure comes from reacting to the market.” -Nick Murray

So… make a financial plan! A financial plan will help you clarify how much cash to keep parked on the sidelines and how much to put to work. A financial plan will provide clarity while keeping your values front and center. Maybe it is bonds, maybe it is stocks, maybe it is to pay off debt? With rates on the move, it is a great time to start a plan, put cash to work, and build confidence about your future.

Follow us on social media below: